by Adam Litster | Jul 4, 2025 | Entrepreneurship Newsletter

Key Qualities of a Top-Notch Bookkeeper and How to Find the Right Fit

In this issue:

- Key qualities of a top-notch bookkeeper

- Must-have credentials & skills

- How they help you succeed

- Tips for finding the right fit

Why a Good Bookkeeper Matters

Think of a bookkeeper as your financial navigator. They guide you through the numbers so you can clearly see where you’ve been, where you’re headed, and how best to reach your destination. With accurate, timely bookkeeping, you’re not left guessing if you can afford that new hire, upgrade equipment, or invest in marketing. Instead, you have solid data that informs your choices, helping you move forward with clarity and confidence.

Beyond just accuracy and timeliness, a great bookkeeper becomes a mentor who helps you understand your financials—and shows you how to use that information to improve both your business and your life.

Key Qualifications to Look For

1. Relevant Certifications & Experience

Look for credentials such as NACPB certification or equivalent, plus a background in accounting or business (often indicated by a college degree). Industry-specific experience reduces onboarding time and increases the value of their insights.

Beware of those who take a quick course and call themselves bookkeepers. Many lack a solid accounting foundation, leading to errors, stress, and costly cleanup for business owners.

2. Attention to Detail & Accuracy

Errors in your records can lead to bad decisions and even legal complications. A top bookkeeper is meticulous—double-checking entries, keeping reconciliations up to date, and ensuring consistency.

Waiting until tax time to tidy up your books leaves you blind to cash flow and profitability until it’s too late. Aim for monthly updates—weekly if possible!

3. Technological Proficiency

Cloud-based tools like QuickBooks or Xero are the norm. A tech-savvy bookkeeper works efficiently, maintains real-time data access, and integrates seamlessly with your other platforms.

4. Effective Communication & Collaboration

Your bookkeeper should explain reports in plain English, listen to your goals, and tailor their support to your needs. Open dialogue builds trust and empowers you to act on the numbers.

Avoid professionals who just email you spreadsheets or restrict your own access. You deserve a partner who guides you through your financials.

5. Forward-Thinking Mindset

Great bookkeepers go beyond reconciling transactions. They highlight spending trends, cash-flow bottlenecks, and high-margin opportunities—providing insights that drive proactive decisions.

How to Find the Right Fit

- Request Referrals from peers, associations, or networking groups to hear firsthand success stories.

- Interview & Ask Tough Questions about deadlines, industry experience, and how they’ll align with your goals.

- Test the Water with a small project or trial period to evaluate responsiveness, accuracy, and communication style.

- Consider Value over Price—very low rates can mean poor quality. Invest in expertise that saves you money and stress in the long run.

- Alternatives: If you’re under $100K in revenue and willing to learn, consider doing your own bookkeeping to build a strong foundation.

Setting the Foundation for Growth

Your bookkeeper plays a key role in building a stable financial base. With the right partner, you’ll gain peace of mind, more time for strategic growth, and confidence that your decisions rest on solid intelligence.

Whether you keep your current bookkeeper, work with our firm, or find someone new, choose the support that accelerates your path to profit and purpose. Let us know if you’d like help finding—and vetting—the perfect fit.

Adam Litster

Certified Profit First Professional and Pumpkin Plan Strategist

(816) 500-5779 | adam@betterbizinfo.com

by Adam Litster | Jun 27, 2025 | Entrepreneurship Newsletter

Business Health Assessment: Five Vines to Strong Growth

In this issue:

- Introducing our new Business Health Assessment (link below)

- The five “vines” of a healthy company—what they are and why they matter

- Why profit must come first before any scaling effort

- How to turn your assessment results into an action plan

Announcing the Business Health Assessment

Entrepreneurs rarely get an objective mirror that says, “Here is what is thriving, here is what is wilting.” That’s why we built the Business Health Assessment. We’ve bundled years of Profit First, Pumpkin Plan, and VPS insights into an online tool that scores your company across five essential areas. In less than five minutes you’ll receive customized feedback plus next-step recommendations.

The Five Vines of Business Health

From Mike Michalowicz’s Pumpkin Plan we learn that a world-class pumpkin grower does not pour energy into every vine—she ruthlessly prunes until one vine receives the lion’s share of nutrients. Your company works the same way. The five key areas are:

1. Sales and Marketing

Healthy companies know exactly who they serve, speak their prospect’s language, and attract leads predictably. Revenue rises from a clear value promise, not heroic discounting or frantic networking.

2. Customer Engagement

Retention beats acquisition every time. Track repeat purchase rate, referrals, and Net Promoter Score. A healthy vine produces raving fans who sell for you while you sleep.

3. Profitability

Revenue is vanity, profit is sanity. When your margin beats industry norms and cash sits in its own account, you buy options: hiring without fear, weathering downturns, and reinvesting into innovation.

4. Employee Engagement

Engaged team members act like owners. Watch voluntary turnover, absenteeism, and idea generation. A strong vine shows people who protect brand promises even when the boss is on vacation.

5. Owner’s Time & Systemization

If the business cannot run for a week without you, you own a job, not an asset. Documented processes, a clear org chart, and calendar space for strategic work are the root system of scale.

Why Profit Comes First

Profit is more than leftover money; it is the scoreboard for value creation and the fuel that powers every next step. When profit is secured up front—by sweeping a fixed percentage of every sale into a protected account—you create three strategic freedoms:

- Decision Freedom – Cash on hand lets you evaluate opportunities on merit, not desperation.

- Time Freedom – With money set aside, you can focus on strategic activities that multiply future profit.

- Resilience – Economic dips, supplier disruptions, or personal emergencies become hurdles, not shutdown events, because you have built a reserve.

A company that locks in profit first can afford the patience required to clarify its unique offering, court premium buyers, and delegate work—all core themes on the path to predictable, sustainable growth.

Turning Results into Action

- Review your scores and highlight the weakest vine—start there.

- Set a 90-day target to strengthen that area.

- Schedule weekly focus time to work on—not just in—the business.

- Reach out if you need help turning the report into a step-by-step plan.

When you know the score and protect profit first, confident growth becomes a choice, not a gamble.

by Adam Litster | Jun 20, 2025 | Entrepreneurship Newsletter

When Progress Snaps Back: Mindset, Financial Triage & the Long-Game

In this issue:

- Why progress often snaps back like a rubber band

- Mindset first aid to protect clarity and courage

- Financial triage steps to stop the bleeding and rebuild trust

- The long-game mindset for digging out of deep debt

Why Progress Feels Like a Rubber Band

Entrepreneurship starts with sparks of possibility—big ideas, bigger dreams, and the promise of meaningful work. But creeping costs, late invoices, and stressful missteps can dim those sparks, turning the dream into a weight you haul uphill. Momentum stalls when cash gaps widen, surprise costs hit, or debt soaks up fresh profit. Without real-time cash visibility and margin buffers, each effort stretches a rubber band that snaps you back to survival mode.

Mindset First Aid

- Capture Small Wins—Write down yesterday’s victories, like a new lead, a completed invoice, or a glowing review.

- Name the Fear—List your worst-case scenarios and assign realistic odds; most threats shrink under light.

- Borrow a Brain—Share numbers with a trusted advisor. Perspective multiplies resilience.

Financial Triage Steps

- Open the Books Fearlessly—List every vendor, balance, due date, and expense.

- Initiate Honest Conversations—Call top vendors, acknowledge delays, and propose a catch-up plan.

- Draft a 13-Week Cash Map—Forecast inflows and outflows weekly; early sight equals options.

- Ring-Fence a Profit Sliver—Move even 1 % of revenue into a separate account to signal your comeback has begun.

- Restructure High-Cost Debt—Explore consolidation or longer terms, then redirect savings to principal.

The Long-Game Mindset

Digging out of months—or years—of late bills and expensive debt is a marathon, not a sprint. Real changes today lay the track for a better future, but results may take three, six, or even eighteen months. Be patient and remember why you started.

If bankruptcy feels imminent, begin by acknowledging reality. Then draft a written, time-stamped, brutally realistic plan. Slash expenses, refine your model, retire low-margin services, or restructure parts of your personal life. Uncertainty shrinks when a plan exists, and anxiety fades with each executed step. Follow it diligently and your comeback becomes inevitable.

Getting Back to Forward Motion

Discouragement thrives in ambiguity. Replace uncertainty with clear data, honest dialogue, and steady action. Track progress, celebrate incremental wins, and recalibrate as conditions evolve. Each deliberate step strengthens footing and restores momentum.

Adam Litster

Certified Profit First Professional and Pumpkin Plan Strategist

(816) 500-5779 | adam@betterbizinfo.com

www.betterbizinfo.com

by Adam Litster | Jun 13, 2025 | Entrepreneurship Newsletter

Perspective That Pays: Stepping Back to Drive Profit and Purpose

In this issue:

- Why nonstop hustle keeps owners lost, not liberated

- Connecting values, vision, and profit into a single internal compass

- Principle-first tactics that break the crisis loop

Why This Matters

If your calendar is full and your mind is tired, profit isn’t the only casualty—your values and vision suffer too. The longer we sprint inside the maze of day-to-day tasks, the easier it is to forget why we started and where we want to finish. That drift shows up as missed family moments, sleepless nights, and a bank account that never seems to match top-line sales.

The Entrepreneurial Pressure Cooker

At first glance the solution seems simple: just sell more. Yet when every new dollar comes with an equal—or larger—cost shadow, revenue feels like pouring water into a bucket with a hole. Popular slogans echo: you must spend money to make money, profits come with volume, owner gets paid last. But these often lead us down a slippery slope that’s hard to escape.

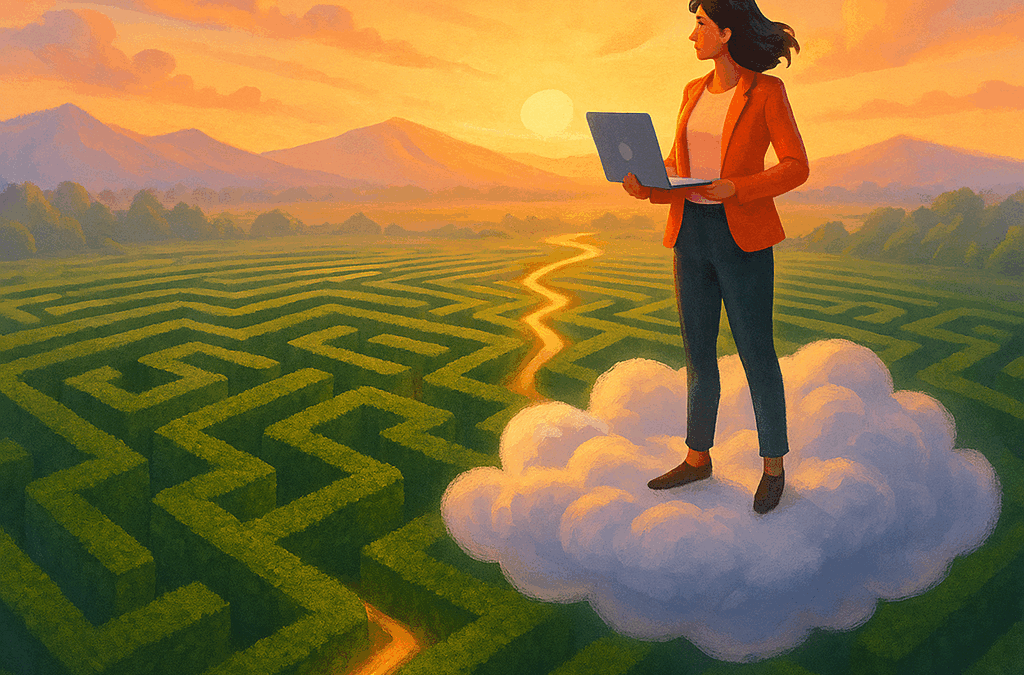

Life Inside the Maze, A Deeper Look

Picture eight-foot hedges stretching farther than you can see. You move down one corridor, hit a dead end, backtrack, then sprint into another wall of green. Time evaporates, and a voice whispers, “Move faster.” Speed inside the maze rarely equals progress.

Now imagine a silent lift carrying you one hundred feet into the sky. The labyrinth flattens into a tidy pattern, and three markers appear:

- The entrance: your original purpose and core values.

- The exit: your ideal life and business impact.

- The optimal path: turns that avoid dead ends and circles.

Stress recedes, because perspective breeds clarity. Inside the maze decisions feel binary and urgent—take a loan or miss payroll, discount or lose the client. Above the maze richer options surface—strengthen margins through efficiency, redirect marketing to your best buyers, refine your service mix to align with core strengths.

Values, Vision, and Profit: Your Three-Point Compass

From the aerial perch you can align three points that refuse to line up when you’re buried in daily fires:

- Values describe the non-negotiable standards for clients, team, and self.

- Vision paints your destination—revenue, lifestyle, impact, and freedom in three to five years.

- Profit funds the trip—the cash that guarantees values stay intact and the vision remains reachable.

When any point drifts, your compass spins. Anchor all three and every choice leads you closer to your ideal life.

Start With One Strategic Hour

Choose a single sixty-minute block this week—phone silent, door closed. In that hour:

- Review Reality: open bank balances, current commitments, and calendar load.

- Reconnect to Compass: revisit your written values and vision, note any drift.

- Identify One High-Leverage Move: tighten a process, reshape your offer for ideal clients, or cut a distracting project.

Anyone can protect one hour. As those moves extinguish recurring fires, expand the practice—ninety minutes, a half-day, eventually an entire Strategy Friday. Each expansion shifts your role from crisis manager to business architect.

Principle-First Tactics That Replace Panic

- Serve the Sweet-Spot Client: focus effort on buyers who respect quality and fit your culture.

- Constraints Spark Creativity: cap operating expenses as a share of revenue before they sprawl.

- Owner Pay Is Non-Negotiable: a business that can’t feed its owner is a hobby, not an asset.

- Kaizen Cash Flow: refine systems continuously—small improvements accumulate into large gains.

- Vision Filters Decisions: if an idea doesn’t move the compass toward the exit, let it pass.

Client Snapshot: From Crisis to Calm

A regional contractor survived for years by chasing any job, creating chaos and thin margins. During their first maze hour the owner saw a mismatch between their core value—craftsmanship—and the low-value projects filling the calendar. By trimming low-margin services, streamlining crew deployment, and requiring deposits before work began, cash flow smoothed and profitability rose—without chasing more volume. Most importantly, the owner reclaimed evenings for family and personal growth.

The Bottom Line

Running harder or faster inside the chaos just gets you to the wrong place faster. Elevate your view, connect values, vision, and profit, and guard one hour this week to begin.

Adam Litster

Certified Profit First Professional and Pumpkin Plan Strategist

(816) 500-5779 | adam@betterbizinfo.com

by Adam Litster | Jun 6, 2025 | Entrepreneurship Newsletter

Debt—Tool or Trap? Understand the Difference Before You Sign

In this issue:

- How inflation and tariff swings drive cash-flow stress

- A payroll-panic story that spiraled into crushing debt

- The three flavors of debt—what they are, real-world examples, and hidden costs

- A three-step plan: freeze new borrowing, build a timing reserve, and eliminate balances with a debt-snowball approach

Why Talk About Debt Now?

With inflation still seesawing and tariffs changing overnight, many businesses feel their cash cushions evaporate faster than expected. We’ve noticed a sharp rise in owners tempted by “instant” online loans or credit-card floats just to cover payroll. Quick cash can feel like relief—until the payments arrive and profit vanishes.

When a Payroll Loan Becomes an Anchor

One client had run lean and profitable—until discipline slipped. Profit and tax transfers paused, expenses crept up, and a $60 k payment from their largest customer came in late. Payroll was due Friday. A Stripe cash-advance offered funds in minutes. Perfect, the owner thought—until the balance lingered and snowballed into multiple high-interest loans that soon became the company’s biggest expense.

Stress and sleepless nights followed—proof that the “quick fix” had become a long-term burden.

The Three Flavors of Debt—Know What You’re Signing Up For

1. Investment Debt—Carefully Calculated

- Purpose: Acquire an asset designed to earn more than the loan costs.

- Example: Financing a new service truck expected to double daily jobs and add $200 k in annual revenue while payments total $120 k. The owner stress-tests the forecast and confirms profits cover the debt even if sales dip 20 percent.

- Why It Can Work: Cash flow from the asset repays the loan and then adds profit.

- Caution: Over-optimistic projections or unexpected downtime can turn a “good” loan into a drag.

2. Timing Debt—Risky, Often Avoidable

- Purpose: Bridge a cash gap between paying expenses now and receiving revenue later.

- Example: A contractor uses a $30 k line of credit to buy materials, expecting payment in 60 days. Weather delays shift payout to 90 days, interest accrues, and the balance sticks. The line of credit becomes semi-permanent.

- Why It Hurts: Interest erodes margins you thought were earned, and balances grow when timing slips.

- Better Path: Build an internal timing reserve so you fund these gaps with your own cash—interest-free.

3. Frivolous Debt—Never Worth It

- Purpose: Cover routine operating costs—payroll, rent, utilities—or factor invoices for quick cash. This debt produces no new revenue.

- Real Outcome: High interest becomes your company’s largest monthly outflow—as painful as adding a second payroll without any new staff.

- Why to Avoid: Adds high fees, masks overspending or underpricing, and compounds stress when payments come due.

Freeze, Reserve, Eliminate—A Principle-Based Plan

-

Freeze New Borrowing and Slash Non-Essential Spend

- Pause new loans and halt discretionary subscriptions for 30 days.

- Negotiate extended terms with key vendors.

- Channel every freed dollar to current balances—think of it as buying back your peace of mind.

-

Build a Timing Reserve—Be Your Own Bank

- Open a separate “Timing” account and transfer 2–5 percent of every customer deposit into it.

- Within a few months, cover material purchases, slow receivables, or minor emergencies with interest-free cash.

-

Eliminate Debt with the Snowball Method

- Choose a weekly “Debt Killer” transfer you can commit to consistently.

- Pay minimums on all balances, then attack the smallest principal first.

- Roll each freed payment into the next-smallest balance to build momentum and boost confidence.

The Bottom Line

In uncertain times, debt can look like the quickest route to calm, but unless it funds a clearly profitable investment, it often amplifies anxiety, drains profit, and steals sleep. Freeze new borrowing, build your own timing reserve, and dismantle existing balances with relentless focus. Your future self—and your balance sheet—will thank you.

Adam Litster

Certified Profit First Professional and Pumpkin Plan Strategist

(816) 500-5779 | adam@betterbizinfo.com

by Adam Litster | May 30, 2025 | Profit First, VPS, Entrepreneurship Newsletter

💡 Tip-of-the-Week

Vendor Call Blitz: Book two 15-minute calls this week asking suppliers for discounts or better terms.

In This Issue:

- Why trimming obvious expenses rarely fixes chronic cash strain

- The “NASA Budget” story and mindset shift

- How to match cost-cutting intensity to your financial health

- Five practical strategies to reach real, lasting profitability

- Tip-of-the-Week ideas to put theory into action

Why This Matters

Most owners begin an expense overhaul by going for the “low-hanging fruit”—cancelling duplicate software, dusty equipment leases, or forgotten subscriptions. We find that most businesses have between 5 and 15% of just waste—expenses that could be cut with no impact on revenue generation. Start by cutting those! That quick 5–15 percent cut feels good—until we find that operating costs still ride at too high of a percentage of revenue (your business expenses should be low enough to provide a healthy profit, pay the owner a good wage, and cover taxes).

After a few rounds of expense reviews you realize, “We’ve already cut the low-hanging fruit—what now?” It often feels impossible to see where else you can cut. This edition addresses the deeper layer of cost control and the mindset needed to uncover it.

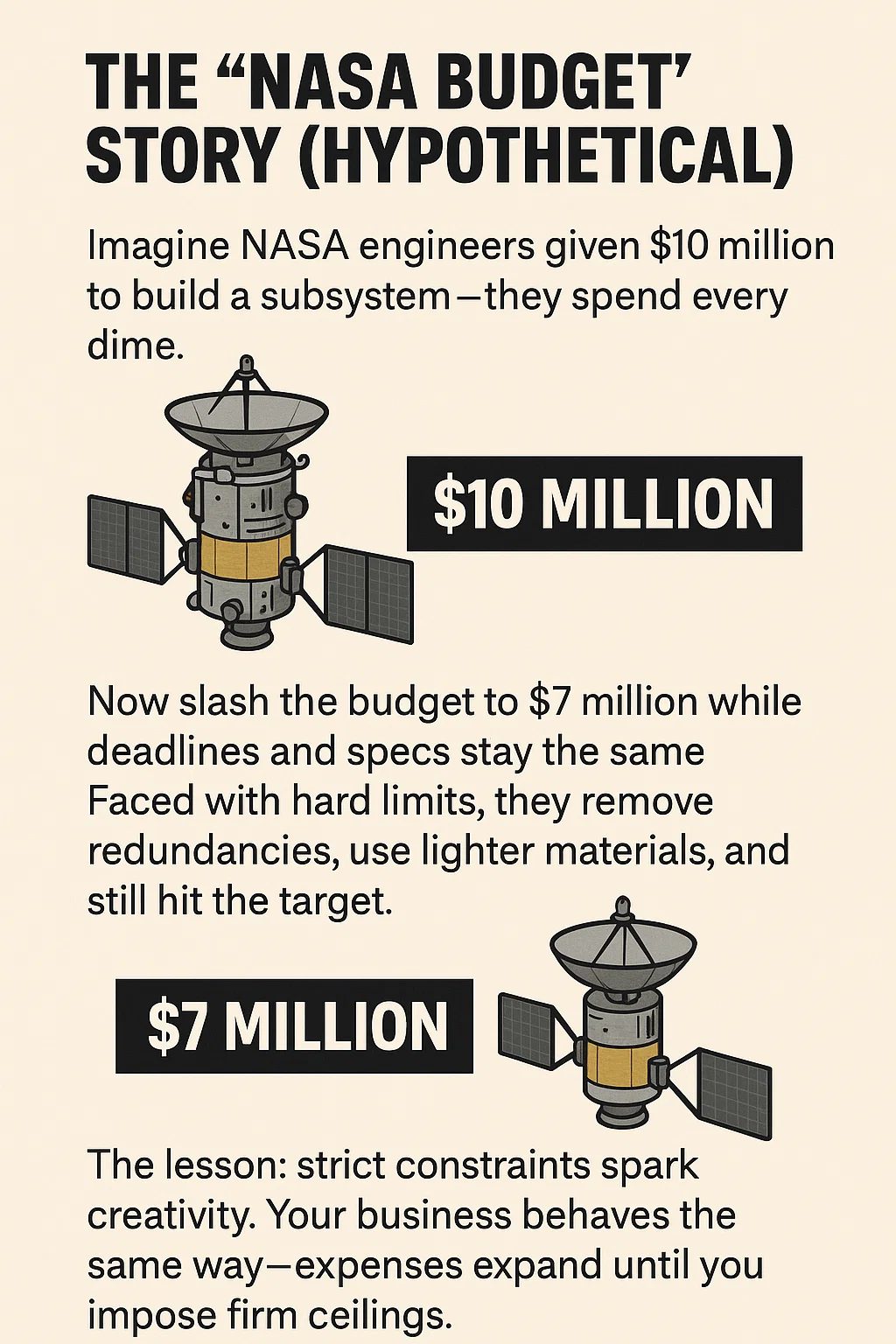

The “NASA Budget” Lesson

Strict constraints spark creativity. Your business behaves the same way—expenses expand until you impose firm ceilings.

Mindset Reset: Redefining “Need”

Entrepreneurs in cash crunches often say, “I need that tool, that software, that employee (or fill in the blank) to run my business.” Ask instead: do you need it more than you need a viable company, a steady paycheck, and peace of mind? Every dollar must earn its keep. If it doesn’t create revenue or protect profit, it’s optional.

Pick Your Intensity: One Size Doesn’t Fit All

Before you dive into strategies for deep cuts or price moves, step back and ask, “How sturdy is my financial house right now?” Your answer guides how aggressively you apply the strategies that follow:

- Crisis Mode — Cash feels like sand slipping through your fingers; payroll is doubtful. You need bold, immediate cuts—pause projects and spending, sublet space, trim non-essential staff. Most importantly — STOP taking out any more debt!

- Survival Mode — Bills get paid but every month is tight. Use a scalpel, not a chainsaw: renegotiate contracts, replace expensive tools with leaner options, raise prices on high-value offerings.

- Improvement Mode — Profitable but below target margins. Focus on small inefficiencies, streamline processes, and double down on high-margin revenue plays.

The weaker your cash position, the stronger the medicine. Align action intensity with urgency so you neither under- nor over-react on the road to lasting profit.

Five Practical Strategies Beyond the Easy Cuts

1. Cut It All—Add Back Slowly

Run a thought experiment: you have zero discretionary budget for 30 days. Add back tools only when their absence blocks revenue. Most firms discover 10–20 percent of costs never return.

2. Cull Low- or Negative-Margin Products

Audit every offering. If it can’t clear your target gross margin, either reprice, bundle, or retire it. Resources freed here fund profitable lines.

3. Pair Aggressive Cuts with High-Margin Revenue Plays

- Upsell existing customers with premium add-ons they already trust you to deliver.

- Incremental price bumps (3–5 percent) on core services often go unnoticed by loyal buyers.

- Strategic alliances: cross-promote with complementary businesses to tap warm audiences at near-zero cost.

4. Systemize to Lower Labor Cost per Unit

Document one repeatable task each week; automate with no-code tools or delegate to lower-cost talent. When labor hours per sale drop, every future sale becomes more profitable.

5. If All Else Fails, Pivot the Model

After radical cuts and margin fixes, if you still can’t fund profit, tax, and a reasonable owner salary, the underlying model is broken. That may mean serving a narrower niche, charging value-based pricing, or launching a new revenue stream with healthier economics.

The Bottom Line

Lasting profitability emerges when you challenge every “need,” match tactics to financial reality, and innovate under constraints—like that hypothetical NASA team. Impose firm limits, rethink assumptions, and watch your business start funding your life instead of draining it.